China is literally down in the financial dumps as billions of dollars of loans it extended to emerging economies in Asia and Africa under the Belt and Road Initiative (BRI) project have turned bad.

According to latest data from Rhodium Group, independent research provider combining economic data and policy insight to analyze global trends, the loans turned sour at a far faster rate than expected as these economies battled the Covid-19 pandemic and inflation.

Nikkei Asia reported that “a total of $76.8 billion in debt was renegotiated — in some cases written off — from 2020 to 2022”, the Rhodium Group data revealed. This figure is more than four times the $17 billion in problem debt for the preceding three years. The first year of the pandemic, 2020, was the worst with $48.7 billion, but the $9 billion in 2022 was still nearly triple the 2019 figure.

Financial Times added: “This is more than four times the $17bn in renegotiations and write-offs recorded by Rhodium in the three years from 2017 to the end of 2019. There are no official figures for the total scale of BRI lending over the past decade, but it is believed to total “somewhere in the ballpark of $1tn”, according to Brad Parks, executive director of AidData at William and Mary university in the US. In addition, Beijing has extended an unprecedented volume of “rescue loans” to prevent sovereign defaults by big borrowers among about 150 countries that have signed up to the BRI.”

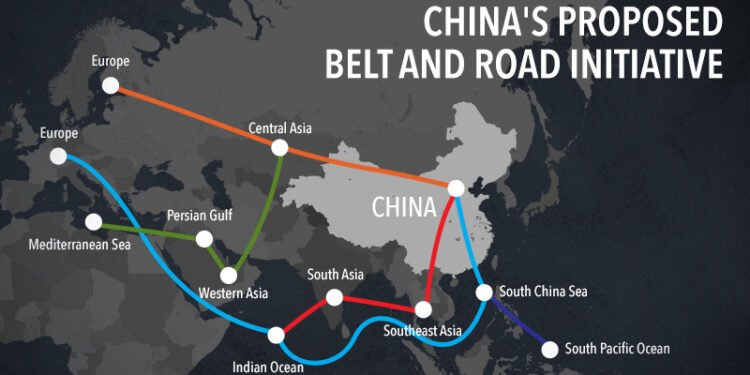

Ever since Xi Jinping came to power and introduced his pet project to project China’s influence across the world through targeted infrastructural financing in developing countries, Beijing backed the construction of ports, roads, railways and other infrastructure from Asia to Africa and Europe.

But over time the investments started turning bad as the countries’ debts began to pile up. Investment came to around $100 billion a year until 2019, but declined amid the pandemic, falling to roughly $60 billion to $70 billion a year from 2020 on, according to data from the American Enterprise Institute.

The loan renegotiations come alongside financial assistance. Of the $240 billion in aid China provided to over 20 emerging markets between 2008 and 2021, about 30% was given in 2020 and 2021 alone, according to research by the World Bank, AidData and elsewhere. Around 70% of the aid came through currency swap lines, giving countries with low foreign exchange reserves access to yuan to repay debts.

A Reuters copy from Johannesburg recently also quoted a study as saying that China spent $240 billion bailing out 22 developing countries between 2008 and 2021, with the amount soaring in recent years as more have struggled to repay loans spent building “Belt and Road” infrastructure. Almost 80% of the lending was made between 2016 and 2021, mainly to middle-income countries including Argentina, Mongolia and Pakistan, according to the report by researchers from the World Bank, Harvard Kennedy School, AidData and the Kiel Institute for the World Economy.

“Beijing is ultimately trying to rescue its own banks. That’s why it has gotten into the risky business of international bailout lending,” Reuters quoted Carmen Reinhart, a former World Bank chief economist and one of the study’s authors as saying.

Chinese loans to countries in debt distress soared from less than 5% of its overseas lending portfolio in 2010 to 60% in 2022, the study found. Argentina received the most, with $111.8 billion, followed by Pakistan with $48.5 billion and Egypt with $15.6 billion. Nine countries received less than $1 billion.

The People’s Bank of China’s (PBOC) swap lines accounted for $170 billion of the financing, including in Suriname, Sri Lanka and Egypt. Bridge loans or balance of payments support by Chinese state-owned banks and companies was $70 billion. Rollovers of both kinds of loans were $140 billion. The study was critical of some central banks potentially using the PBOC swap lines to artificially pump up their foreign exchange reserve figures.

Take the case of Sri Lanka in Asia which nearly reached its economic nadir last year resulting in people almost revolting against the government unable to face shortages and price rise. The country drove itself into a crisis because of swelling external debt from China it could not handle. When Sri Lankan creditors met recently to restructure the debt, China took part in the meetings as an ‘observer’.

It is not that the bad loans will financially destabilize China. The country has the world’s largest foreign exchange reserves, nearly $3.2 trillion this April. Though much of it is tied up in lending to developing countries, it may pull through in the short run unless its financial system is unable to handle the strain. The hurt is more to the communist leadership’s ego as the massive BRI plan now appears to be sinking in a quagmire of its own making.

Chinese corporate and retail bank accounts saw net outflows from overseas transactions for a second straight quarter in the three months through March, amid a slump in exports. If the trend continues, China could have less capital to lend overseas. Beijing’s push to develop industries such as semiconductors to compete with the US also could pull resources away from Belt and Road lending, media analysts say.

According to a media report, Italy, the only Group of Seven country involved in the initiative, is distancing itself. A senior official told Reuters this month that Rome is unlikely to renew the agreement with China when it expires in early 2024, but added that more time was needed for talks with Beijing. Critics say the deal has failed to bring the anticipated boost to economic growth for Italy, with exports to China seeing sluggish growth compared with imports.

Stung by western criticism of trying to take undue advantage of financially weak countries to project its influence, China hit back its investments operated on ‘the principle of openness and transparency’.

“China acts in accordance with market laws and international rules, respects the will of relevant countries, has never forced any party to borrow money, has never forced any country to pay, will not attach any political conditions to loan agreements, and does not seek any political self-interest,” Mao Ning, foreign ministry spokesperson, said at a news conference.

According to the report, the bailout loans are mainly concentrated in the middle-income countries that make up four-fifths of its lending, due to the risk they pose to Chinese banks’ balance sheets, whereas low-income countries are offered grace periods and maturity extensions.

China is negotiating debt restructurings with countries including Zambia, Ghana and Sri Lanka and has been criticized for holding up the processes. In response, it has called on the World Bank and International Monetary Fund to also offer debt relief.

{kind=link}